Fixing the Duck Curve in California (Video)

The Future of California’s Energy Market (Video)

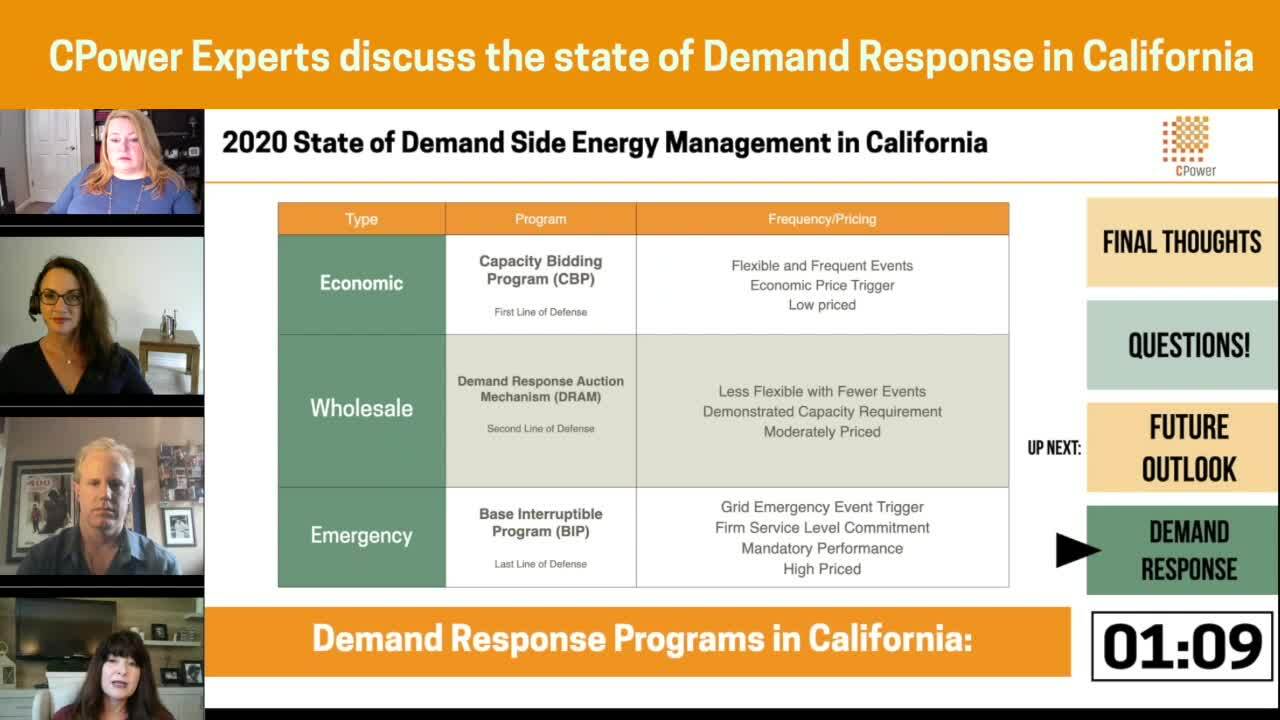

The State of Demand Response in California’s Energy Market (Video)

Golden State Chaos – The State of California’s Energy Market (Video)

State of the 2020 California Energy Market (Webinar)

The Golden State’s energy market was poised to have a wild ride in 2020 before the onset of COVID-19 and the ensuing lockdown. As California now works its way through the pandemic’s maze, organizations are reexamining their energy management strategies in search of optimization for an increasingly uncertain future.

Topics covered include:

- Policy and regulatory changes in California

- An update of the state’s renewable pursuits

- Opportunities to monetize storage and other energy assets

- Maximizing returns on demand response in CAISO and CA utility programs

- And more…

CPower’s California energy market experts Jennifer Chamberlin, Laura Jelin and Diane Wiggins host this webinar that includes a question and answer session.

SOTM 2020 Webinar Series

60 minutes with CPower Experts. Energy Insights to Plan Your 2020…

CPower Experts Share Insights Into North America’s Energy Markets in 2020 (Webinar)

Watch the latest webinar from CPower and SED

2020 State of Demand-Side Energy Management in North America

Last year, nearly 2000 organizations nationwide downloaded the State of Demand-Side Energy Management in North America book by CPower’s energy experts.

This year, we pick up where we left off with a market-by-market analysis of the issues, trends, and regulations organizations like yours should understand in 2020 to make better decisions about your energy use and spend.

What’s Driving Energy Prices in California?

Wet year. Low energy prices.

In 2019, California’s energy prices were low, driven, in part, by the fact that it was a wet year in the West. The abundance of available snowmelt and surface water allowed for hydro facilities to generate what would otherwise have to be delivered by more expensive generation units. In dry years, 2014 for example, hydro facilities simply can’t run as often as they do in wet years and the need for marginal generation resources increases, thereby resulting in higher energy costs.

As of this writing, it is too early in the state’s water year to predict whether 2020 will be as wet as 2019 and yield similar prices as last year. In January 2020, roughly the midpoint of the current water year, California’s Department of Water Resources reported that eight of its 12 reservoirs were at or above historical average levels, with none below 91% of normal.

Low energy prices. High resources (For now)

While electricity rates in California have been traditionally high, wholesale energy prices have been low. The average cost per megawatt-hour of load decreased 44 percent to about $39/MWh for the third quarter of 2019 from $69/MWh in the same quarter of 2018. The decrease in average wholesale electric prices has been primarily driven by a 43 percent decrease in natural gas prices compared to the same quarter in 2018.

Currently, as was the case in 2019, California as a whole is an over-resourced state due to its profusion of resources on the grid that have been built to keep up with the expanding Renewable Portfolio Standards (RPS) requirements. That abundance, however, appears to be changing.

In its annual Resource Adequacy Report released in August 2019, the CPUC identified (for the first time, on record) a shortfall in system resources. The overall available capacity that can be used to meet all load-serving entities’ (LSE) resource adequacy (RA) decreased significantly due to the retirement of 3,122 MW of older gas cogeneration facilities. Increased penetration of use-limited resources on the grid has also raised RA concerns.

To alleviate the shortfall, California’s Integrated Resource Planning (IRP) and CPUC ordered 3.3 GW of system RA to be procured by all LSEs (IOUs, CCA’s and Electric Service Providers) under the CPUC’s jurisdiction and to come online between August 2021 and August 2023. Considering the California grid typically runs at about 35 GW on a non-peak day, the 3.3 GW order is substantial.

Does the current Resource Adequacy Program pass muster?

Faced with rapidly changing resource dynamics on the grid, the CPUC is conducting a regulatory proceeding to evaluate the RA program to determine if it meets the needs of California’s evolving grid. Questions the commission seeks to answer include:

- Will the current and projected resource mix ensure grid reliability?

- Will CA have enough energy available during all hours?

- What changes (if any) in counting of availability limited resources–including renewables, storage and demand response–are needed?

- Should local RA be procured centrally to ensure local reliability? If so, by whom?

- Should the flexible RA construct be adjusted?

The ongoing evaluation and subsequent debates will be a major issue to watch in 2020-2021. What results could ultimately affect the capacity valuation and participation rules of customer-sited resources including solar, storage, and demand response–both behind the meter and/or in microgrid configurations.

This post was excerpted from the 2020 State of Demand-Side Energy Management in North America, a market-by-market analysis of the issues and trends the experts at CPower feel organizations like yours need to know to make better decisions about your energy use and spend.

CPower has taken the pain out of painstaking detail, leaving a comprehensive but easy-to-understand bed of insights and ideas to help you make sense of demand-side energy’s quickly-evolving landscape.

The Challenge of Valuing DERs in California’s Energy Market

On its website, the CPUC states that the Resource Adequacy program “is designed to provide appropriate incentives for the siting and construction of new resources needed for reliability in the future.”

So what’s the problem?

Many energy professionals in California would argue the state’s inability to properly value DERs in the marketplace is stymying innovation and evolution on the state’s grid that would otherwise take place.

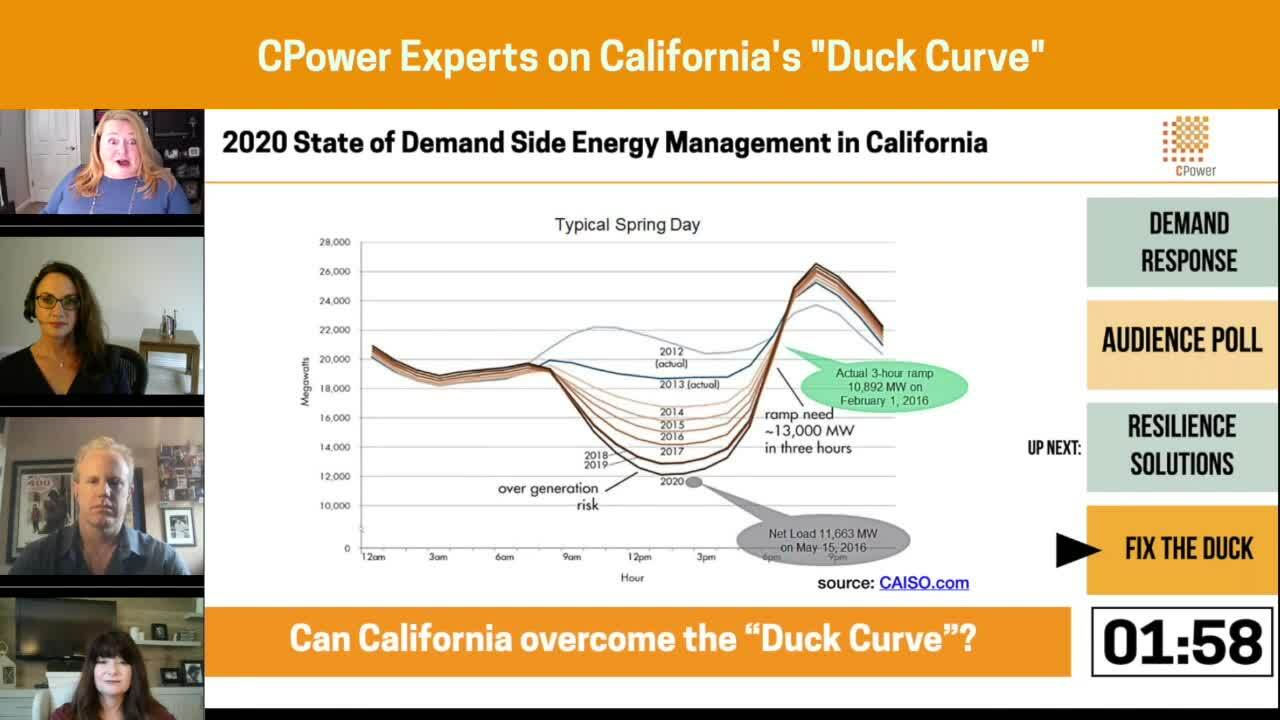

In California, a given resource’s capacity value is determined by the resource’s ability to either generate or curtail in response to grid operator direction. For demand response programs, this is measured as their ability to curtail during the CAISO’s established availability assessment hours. These hours coincide with when the grid is most likely to need extra capacity–namely, in the evening as the sun sets and the state’s solar supply goes offline and residential consumption spikes as people come home from work and go about their electricity-powered lives.

Renewable energy sources such as solar are inherently intermittent. Their supply is not continuous or steady. Solar, of course, is only viable during (cloudless) daylight hours.

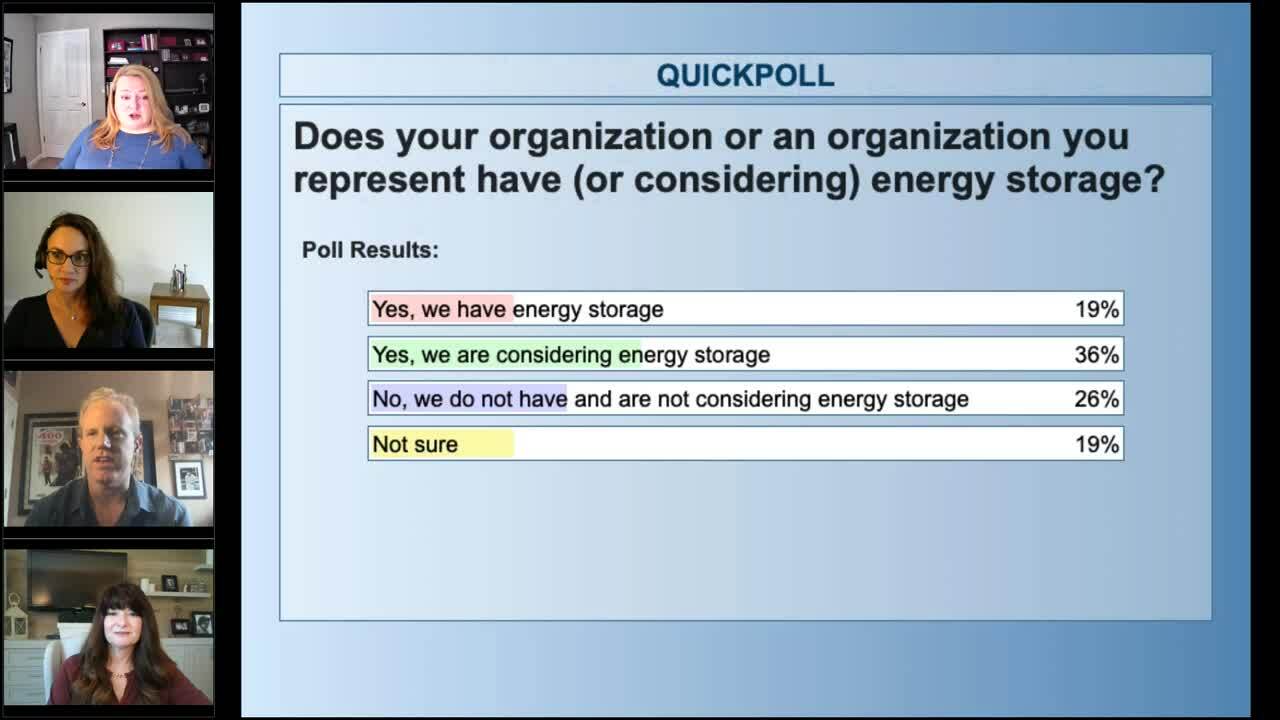

California has been a leader in creating hybrid energy resources that combine distributed energy resources (including renewables) with energy storage.

So far, so good for the Golden State. Here’s the problem.

While customer-sited, behind-the-meter hybrid resources may participate in California’s wholesale energy market as part of demand response, hybrid resources that consist of front-of-meter resources–as are often found in microgrids–are not fully valued by the CPUC as resource adequacy.

Consider a front-of-the-meter solar resource that qualifies as resource adequacy. If the owner of that asset were to add an energy storage resource, the ensuing Qualifying Capacity (QC) value (essentially the MW value that can qualify as RA) would change and thereby cancel the value benefit of the combined resource. Hybrid resources, therefore, are either kept out of the marketplace or they are significantly undervalued.

This situation keeps increasingly popular resilience resources on the sidelines instead of supporting grid needs and allowing for them to monetize their value when not providing support to the customer for daily or Public Safety Power Shutoff events (PSPS).

As we suggested in the introduction of this book, renewable resources packaged with demand-side resources such as energy storage and demand response may be a panacea for evolving grids and markets seeking to integrate renewables and overcome their inherent intermittency issues.

Yet, California–the longtime global leader in renewable energy innovation–is lagging behind other US energy markets when it comes to devising a plan to value many DER resources in the marketplace. As a result, the Golden State’s march toward energy’s future has slowed while these issues work toward a resolution.

The state has ample clean energy capacity available to meet its RA requirements now and in the future in accordance with the established goals of the RPS. Unless, however, those renewable resources when packaged with energy storage and/or demand response (hybrid resources) are permitted to both qualify for the RA program and participate in the wholesale market, the standstill will likely continue. For how long depends on whether the CAISO and CPUC can work together in 2020 to establish rules and regulations to allow resources to harness available and developing value streams.

Will 2020 be the year of proper valuation for DERs in California?

That’s the million-dollar question. Depending on your organization’s energy asset portfolio, the question may be worth a lot more.

And now is as good a time as any to remind that predicting when market-altering legislation might be introduced is the ultimate fool’s errand in the energy industry. But since you picked up this book looking for answers to the million-dollar question, we might as well play the fool and make a prediction.

Will 2020 be the year the CPUC and CAISO agree on how to qualify and value DERs in the retail and wholesale markets in a way that inspires innovation and implementation on both the supply and demand side?

Not likely.

Simply put, too much has to happen and neither party has made the kind of progress to suggest a sensible plan can be introduced, approved, and implemented this year. But that doesn’t mean that organizations should throw up their hands, bury their heads in their utility bills and wait for next year.

This post was excerpted from the 2020 State of Demand-Side Energy Management in North America, a market-by-market analysis of the issues and trends the experts at CPower feel organizations like yours need to know to make better decisions about your energy use and spend.

CPower has taken the pain out of painstaking detail, leaving a comprehensive but easy-to-understand bed of insights and ideas to help you make sense of demand-side energy’s quickly-evolving landscape.