CPower signs contract with PECO to help business customers in Pennsylvania reduce electricity demand during peak hours

CPower signs contract with PECO to help business customers in Pennsylvania reduce electricity demand…

Understanding kW vs kWh (and Meter Data) to Lower Your Utility Bills

Many customers as well as my colleagues at CPower often ask me about the benefits of installing reliable metering equipment to access energy data in near real time. I typically respond with a handful of advantages (some listed below), but even before going there I find it useful to explain the full context about why these are important.

No discussion on the topic would be complete without a basic understanding of Demand (measured in kilowatts or kW) versus Consumption (measured in kilowatt hours or kWh). This is key to making the right choices when it comes to reducing energy costs, since electricity use for a commercial/industrial customer is typically billed and metered after taking at least these factors into consideration:

- Maximum kilowatt use (or kW demand) during a given period, typically in 15- or 30-minute intervals, and

- Total cumulative consumption (in kWh).

So, what’s the big deal between kW vs kWh?

An analogy using traditional light bulbs can help: Consider a single 100W bulb lit for ten hours versus ten 100W bulbs lit simultaneously for one hour. In both scenarios, the total cumulative “consumption” is 1,000 watt-hours (or 1 kWh). In the first case, however, the single light bulb will “demand” 100W or 0.1 kW from the electric supplier. Thus, the utility must have that 0.1 kW ready whenever that bulb is switched on. But note how the second scenario impacts the utility from a “demand” perspective. The electric supplier in this case must be ready to deliver 10x as much ‘capacity’ in response to the demand of the 10 light bulbs burning simultaneously!

Quite simply, here’s the difference. If these two scenarios reflected the behavior of two different customers, and if they were each billed for only their consumption, then both would get the same bill (for 1 kWh of energy used) even though the burden placed on the utility to meet each customer’s energy requirement is very different. Among other reasons, this is primarily why C&I (as opposed to residential) customers are typically metered and billed based on both their hourly “consumption” patterns and their peak “demand” for energy.

Demand-side energy management in near real time

CPower’s savvy demand response (DR) customers effectively leverage the energy they consume as a facility asset. Our diverse customer base covers mid- to large-sized electricity users in commercial, industrial, government and institutional organizations, including water/wastewater pumping and treatment facilities, colleges and universities, public agencies, office campuses, cold storage, data centers and a wide range of manufacturing facilities, to name just a few.

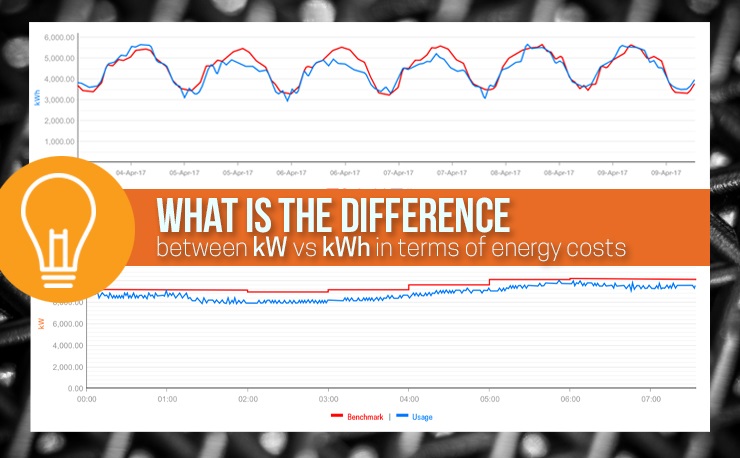

Many of our most active DR participants nationwide additionally leverage real-time metering for its clear advantages, including more visibility and control over load reductions as well as better overall energy management and sustainability benefits. The image above shows just two of the many views available to users via the CPower App (the graph on top shows 7-day hourly interval consumption while the one below shows demand on an intra-day 1-minute interval chart).

Key reasons to get real-time metering installed at your facility:

- You can identify unusual or erratic equipment behavior to help avoid catastrophic failure. This is from a recent real-world example: Our team at CPower was working with the operations team for a large commercial real estate and property management firm, and picked up on unusual/erratic daytime usage patterns at one of their facilities. A look at the major systems of the building revealed that a chiller which had been recently serviced was to blame. Further investigation revealed that during a recent service call the chiller had been severely over-charged with refrigerant. Having a near real-time window into their energy usage enabled the facilities personnel to identify the unusual usage pattern, and proactively remedy a potential chiller issue that could have resulted in thousands of dollars in repair costs and possibly escalated their demand charges had it gone unnoticed.

- Similarly, you may discover unusual, wasteful patterns or aberrations in overall facility energy usage as well as specific areas (e.g., an BAS reset inadvertently switches on all lights in an unoccupied underground parking garage at 2 AM).

- Simplify on-site event planning (e.g., for K-12 schools or colleges) and/or production line scheduling (for manufacturing) with day-ahead pricing and forecasting at your fingertips.

- Quickly and accurately substantiate the impact of your energy efficiency initiatives and sustainability programs (and share results with your team and management).

- Avoid setting a new annual or monthly consumption peak, enabling you to manage demand charges for next year. Click to see more on Peak Demand Management in New England and Texas, for example.

- Immediately evaluate the efficacy of (and fine tune as needed) new load curtailment strategies.

- Further leverage your building automation systems and curtailment planning while minimizing impact on occupants (students, staff, employees, tenants, etc.).

- Facilitate optimized participation in multiple DR programs, including Emergency Capacity, Economic DR, Ancillary Services, and more.

- In addition to monitoring real-time utility load, several customers (i.e. a manufacturer of water valves and a supplier of military components) also view sub-meter data in the CPower App to provide them with a more granular, process-level picture of the energy usage in their facility.

The Bottom line

Real-time metering ultimately increases your DR earnings and savings to fund additional efficiency initiatives, while complementing your facility’s energy conservation and sustainability efforts. There are no out-of-pocket costs, since fees to install hardware, support software provisioning and enable data measurement & verification (M&V) are typically covered by DR program earnings.

By giving you near real-time visibility and analytics of your energy consumption, enhanced metering techniques provide more earnings and savings via greater control over your DR participation and greater awareness of electricity usage patterns (remember kW vs kWh!)

ERCOT DR

CPower can help you earn with ERS and LR and save with 4CP…

Texas Generators

You rely on your backup generator for power when there’s an outage.…

CPower to help reduce electricity demand during peak hours in National Grid’s New England service territory

CPower to help reduce electricity demand during peak hours in National Grid’s New England…

NE Generators

CPower’s team of energy experts can assess your generator and determine if…

New England Demand Response

CPower can help you earn with Real Time Demand Response and…

Program Snapshots

Key information on demand management programs around the country. Learn…

PECO Demand Response

Why should you consider the Act 129 Demand Response…

Eversource Demand Response Resources

Capacity prices are rising .…